I had started writing this article a week ago but was not really sure what I was conveying and then this article (Death of a Salesforce) from Andreesen Horowitz came out and it highlighted what I was feeling. While their article focused specifically on Sales Tech and specifically Salesforce / Hubspot, I think there is a bigger hit coming at SaaS companies.

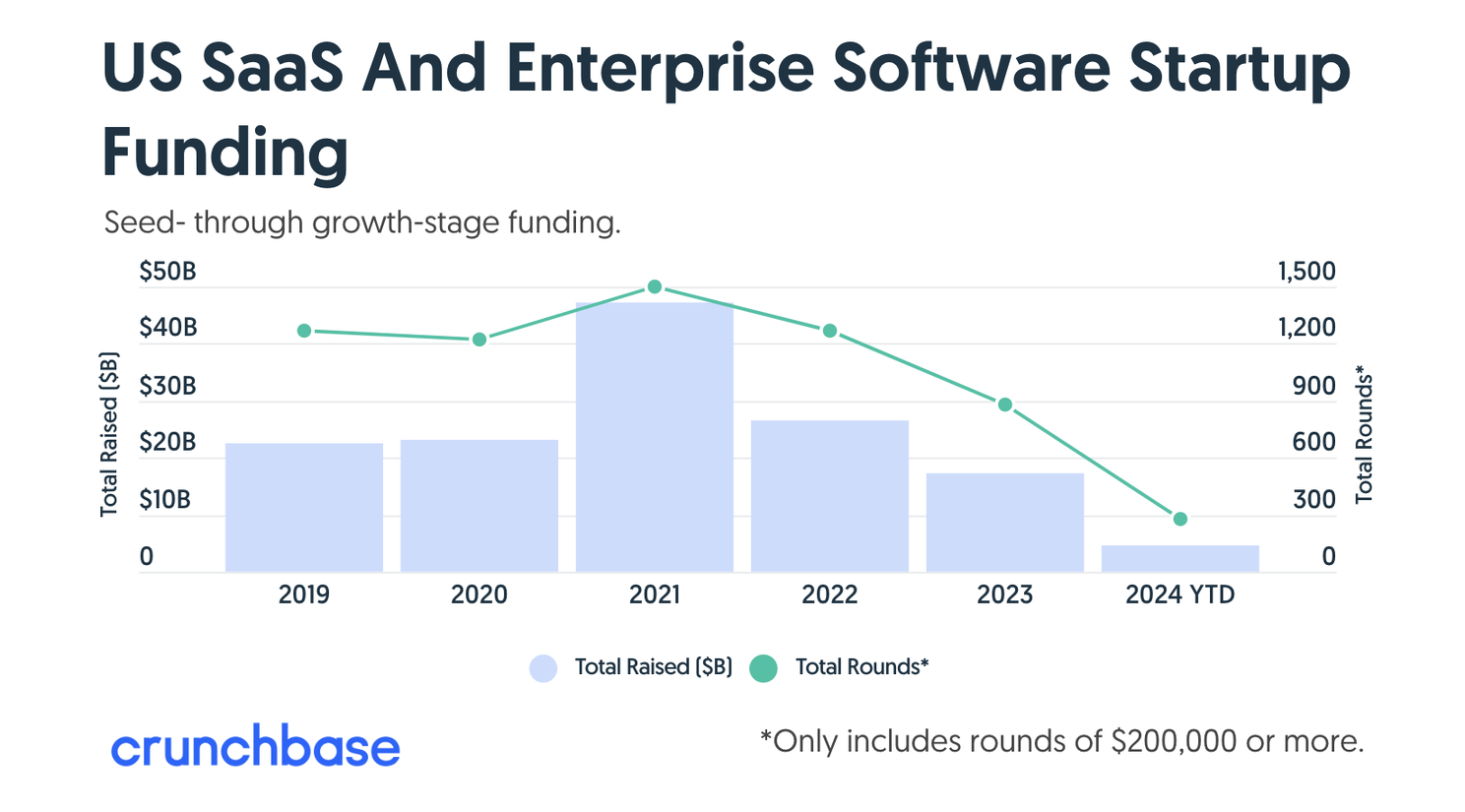

It is an understatement to say that SaaS is in a bit of funk. VC funding is way down from the highs of 2021 - That puts 2024 on track to come in far below last year’s $17.4 billion annual tally — which was itself the lowest total in years

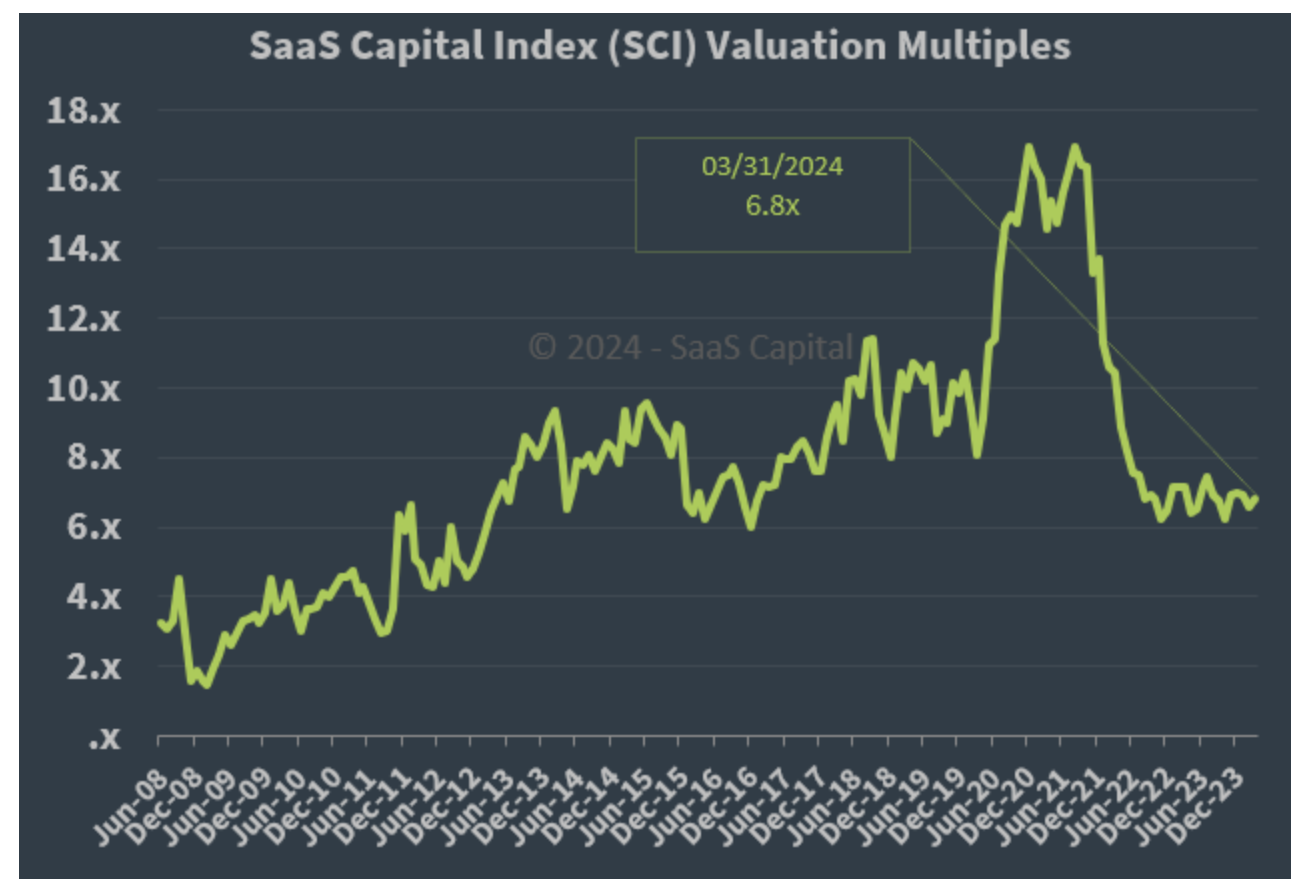

SaaS valuations are way down - While the multiple has stabilized in the 6-7x range, it is down roughly 60% from its peak achieved in 2021.

The Cloud Computing ETF is way down from its highs. In 2021 it was at 31.64 and today it is at 19.78.

No wonder we see questions like - Is SaaS dead?

It reminds me of a statement Tom Walker, CFO of Tableau, made when I joined Tableau in 2013. He said that Tableau was a 'Cloud only' vendor. All the software they used was cloud based and SaaS. They had no on-premise software (technically there was some SQL Server but that eventually moved to Snowflake). I had just joined Tableau from Microsoft and prior to that I had been at Oracle. Needless to say all the software they had was on premise (Azure had just come out, O365 had just come out).

It's fair to say that SaaS had a 10-15 year golden run. Organizations now have tons of SaaS applications. If you have a need, there is a SaaS application for that.

The hot new trend now is GenAI. As this article said it - GenAI is churning out unicorns like it is 2021. It is fair to say that a lot of the VC money has moved from SaaS to GenAI. While a lot of the VC money is going to the GenAI infrastructure players (OpenAI, Anthropic etc.), there is money going into pure play GenAI startups that resemble SaaS applications. The big difference is that they are built with GenAI at the core as opposed to SaaS applications that are adding GenAI functionality.

So in some ways, VCs are funding competitors to existing SaaS vendors while stifling funding to existing SaaS vendors. Add to this the inability for existing SaaS vendors to charge extra for GenAI features and it is a double whammy for SaaS. Costs are going up, funding is not flowing in and revenue from GenAI is not coming in.

The other big challenge is that GenAI is bringing in a new architecture that someone building on from the ground up will have an advantage over legacy SaaS vendors. Legacy SaaS vendors have a legacy architecture that costs money to maintain and can only bolt on GenAI to. Legacy SaaS vendors have to pay a bunch of developers to maintain that legacy application. Legacy SaaS vendors won't have the deep pockets to rewrite their applications from the ground up leveraging GenAI (or the ones like Salesforce that do, will waste a lot of money on this effort).

What does this new architecture look like - I don't know the answer to this but early signs point to natural language interfaces, agents that run tasks and workflows, LLM functionality in the core of the application etc. When I see applications like letter.ai and tribyl.com, I see the beginnings of a new type of application.

It is going to be an interesting rest of the decade and I am very curious to see what happens to the various SaaS startups that are pre-IPO and those that are post-IPO and what the new generation of GenAI based applications is.